There was a period when choosing among liquid staking platforms was a straightforward yield comparison. You looked at APY, you looked at fees, and you picked the highest number. That assumption is now structurally obsolete — and the speed at which it has become obsolete is the story most market participants have not yet internalized.

Table of Contents

The Solana DeFi stack is no longer a collection of independent protocols that happen to interoperate. It is converging into a unified financial layer where staking, lending, liquidity provision, validator operations, and ecosystem tooling are structurally interdependent. The liquid staking token — and the platform that issues it — sits at the center of this convergence. Understanding why changes how you evaluate every liquid staking crypto decision going forward.

The Stack Is No Longer Modular — It’s Structural

The original mental model of Solana DeFi was modular: a staking layer, a lending layer, a DEX layer, each operating independently with composability as an optional bridge between them. That model described 2022. It does not describe 2026.

What has changed is not the technology — SPL tokens were always composable. What has changed is the incentive architecture. Liquid staking platforms are no longer simply minting yield-bearing tokens and letting users figure out what to do with them. The platforms themselves are now structurally embedded in the protocols their tokens touch.

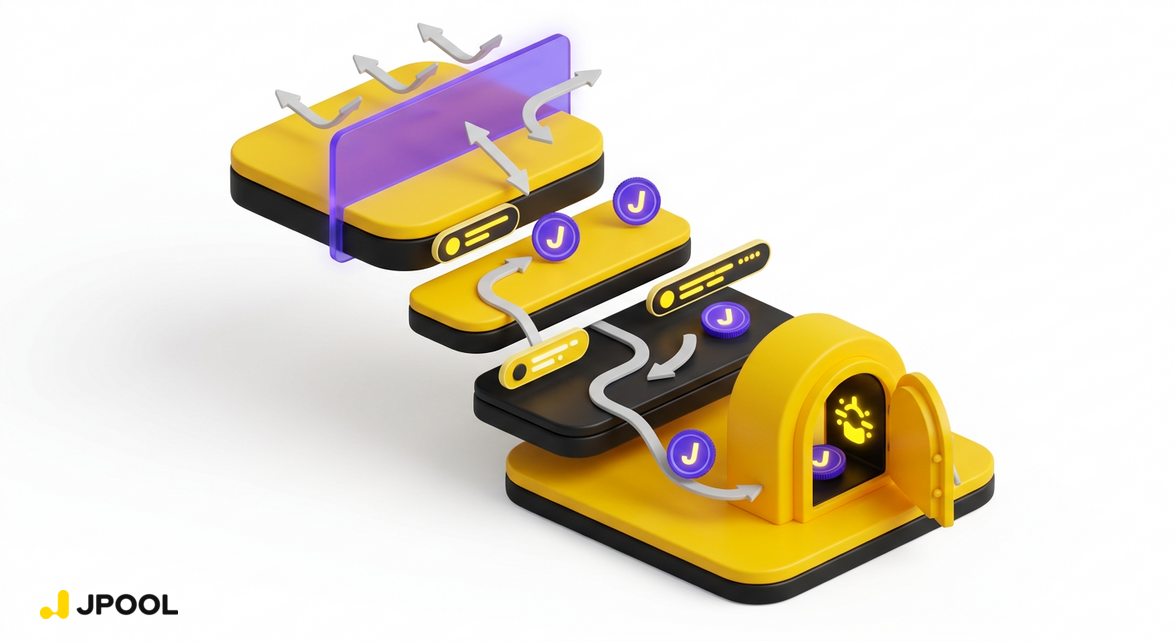

JPool’s documentation makes this explicit in its description of the delegation strategy’s self-reinforcing cycle:

“More validators attract direct stake → more SOL flows into JSOL → deeper DeFi liquidity → JSOL becomes more useful → more stakers choose JPool → more TVL → more validator slots → broader decentralization → stronger network.”

This is not a marketing tagline. It is a description of a closed feedback loop where each layer of the stack actively strengthens every other layer. The liquid staking platform is no longer a product sitting on top of the stack — it is load-bearing infrastructure running through the middle of it.

The Flywheel Nobody Drew a Map Of

The convergence becomes most visible when you trace the full circuit of how stake, liquidity, and validator health are now co-dependent.

- Validators need liquid stake to compete. JPool’s delegation model scales its validator set linearly with TVL — one validator slot per 10,000 SOL. This means that as more SOL flows into JSOL, more validators receive meaningful delegation. Validators who attract direct delegators receive proportional matching from JPool, making every delegator worth 1.5 to 2x more through the matching mechanism. The validator’s growth is now structurally tied to the liquid staking platform’s TVL growth.

- DeFi protocols need deep JSOL liquidity to function. Lending platforms like Save and Kamino accept JSOL as collateral precisely because it is a yield-bearing asset with sufficient liquidity depth. That liquidity depth is itself a function of how many stakers hold JSOL rather than native SOL — which is a function of how useful JSOL is in DeFi. The circularity is intentional: the more protocols accept JSOL, the more valuable JSOL becomes as a DeFi asset, which draws more stakers, which deepens liquidity, which makes JSOL more attractive to protocols.

- The bond system bridges stakers and validators into a single guarantee. JPool’s bond mechanism — where every validator in the delegation program posts collateral that covers both security risks and APY shortfalls — means that delegators are guaranteed the Target APY regardless of individual validator underperformance. The Target APY is recalculated every epoch based on the mean APY of the top 30 mid-size validators on Solana. This is not a feature of the staking layer in isolation — it is a structural coupling between validator economics and staker outcomes that did not exist in the native staking model.

The result: a delegator staking through JPool is simultaneously a participant in the lending market (via JSOL collateral), a contributor to validator economics (via matching amplification), and a beneficiary of a yield guarantee backed by validator bonds. These are not separate relationships. They are one position.

Where Convergence Creates Selection Pressure on Liquid Staking Platforms

The convergence of the stack creates a new selection criterion for liquid staking crypto that has nothing to do with base APY: infrastructure depth.

A liquid staking platform that issues a token but does not actively manage the validator layer, the DeFi integration layer, and the tooling layer is now at a structural disadvantage. The token it issues will have shallower DeFi liquidity, weaker validator guarantees, and less ecosystem utility — all of which feed back into lower TVL, which feeds back into fewer validator slots, which feeds back into weaker network effects.

JPool’s approach to this selection pressure is visible in the tooling layer it has built around the token:

- Smart Validator Toolkit (SVT): An all-in-one validator cockpit that automates node bootstrapping, monitoring, alerting, and analytics. SVT is not a staking product — it is infrastructure that strengthens the validator layer that JSOL depends on.

- JPool Insights: A transaction tracking and reporting tool that provides real-time monitoring of staking-related transactions, detailed reporting for accounting purposes, and token portfolio tracking. This is the transparency layer that institutional participants require before treating JSOL as a balance-sheet asset.

- Validator Dashboard: A comprehensive interface providing uptime, commission rates, and stake pool data for both operators and delegators — the information layer that makes delegation decisions rational rather than opaque.

- Validator Profit Calculator: An interactive tool for estimating validator profitability across different time horizons, enabling what-if analysis on commission, stake, and performance assumptions before changing settings.

None of these tools exist in isolation. Each one strengthens a different layer of the stack that JSOL depends on — and each one creates a reason for validators, delegators, and institutional participants to remain within the JPool ecosystem rather than migrating to a platform with a shallower infrastructure footprint.

The Infrastructure Commitments Beneath the Token

The deepest form of convergence is not visible in the token itself. It is visible in the structural commitments the platform makes to every participant in the stack.

JPool’s documentation states that it maintains a minimum reserve of 0.5% of TVL (at least 5,000 SOL), with a 1% target (at least 10,000 SOL), to ensure stakers can always withdraw. This reserve is not merely a staking feature — it is a structural commitment to the liquidity layer that makes JSOL usable as collateral in lending protocols. Without a predictable reserve floor, lending protocols cannot safely set collateral parameters for JSOL, which limits its utility, which reduces DeFi demand, which weakens the flywheel.

Similarly, the bond system’s Target APY guarantee — recalculated every epoch from the top 30 mid-size validators — creates a floor under staker returns that makes JSOL a more predictable yield instrument than native staking. Predictability is exactly what DeFi protocols require when pricing JSOL as collateral. The bond system is, in this sense, not just a validator accountability mechanism — it is a DeFi infrastructure feature.

This is the layer of convergence that most discussions of liquid staking crypto miss entirely. The question is not just “what yield does this token earn?” It is: “what structural commitments does the platform make to every participant in the stack that this token touches?”

What Unified Infrastructure Means for the Best Liquid Staking Crypto Decision

The convergence of the Solana DeFi stack changes the evaluation framework for liquid staking platforms in three concrete ways.

- First, TVL depth is now a proxy for DeFi utility, not just platform size. A platform with deeper TVL supports more validator slots, deeper DeFi liquidity, and stronger lending market integration. JPool’s linear scaling model — one validator slot per 10,000 SOL of TVL — means that TVL growth directly translates into network decentralization, which is itself a DeFi infrastructure feature.

- Second, the validator layer is now a DeFi risk factor. A liquid staking platform whose validator set is opaque, unguaranteed, or concentrated is introducing validator risk into every DeFi position that uses its token as collateral. JPool’s bond system, commission cap, and stake concentration limits are not just staking features — they are risk parameters for every lending protocol that accepts JSOL.

- Third, tooling depth is now a competitive moat. SVT, JPool Insights, the Validator Dashboard, and the Validator Profit Calculator are not ancillary products. They are the infrastructure that keeps validators, delegators, and institutional participants within the ecosystem — and that ecosystem depth is what makes JSOL a more durable DeFi asset than a token issued by a platform with no tooling layer.

The best liquid staking crypto in a converged stack is not the token with the highest point-in-time APY. It is the token issued by the platform most deeply embedded in the stack it participates in — because that embeddedness is what makes the token’s yield, liquidity, and collateral utility durable rather than fragile.

For a deeper look at how JSOL participates in DeFi loops and lending integrations, see Designing Capital-Efficient DeFi Loops with Liquid Staked SOL. For the broader context of where liquid staking is heading — including restaking and shared security layers — see The Next Phase of Liquid Staking: Restaking, Shared Security, and New Yield Layers. And for a precise understanding of how exit liquidity works within this converged stack, see Understanding Redemption Liquidity in Liquid Staking Pools.

Start building your position at jpool.one.

Subscribe to our digest pages and stay updated:

Leave a Reply